Part Three of a Three-Part White Paper Series

By Thomas Ricketts, CFA

The Power and Limits of Mental Models

The Evolutionary Investing framework and the Technology and Industry Evolution Model I have outlined in previous white papers delineate the long and winding path of an invention and generational progress of technologies. This model may give the impression that every new technology will progress neatly through each phase of the model, that there will be smooth, if not linear, progression from one phase to the next, or that each technology or innovation will be successful. Intellectual integrity leads me to make clear that these would be incorrect takeaways and that, while the model has great utility, it also, like any mental model, has limitations. Thus, the application of the model must be applied with great care and a focused, dedicated research effort.

We use mental models every day, knowing they have limits as well as great power. One of the major contributions of Charlie Munger, the long-time partner of Warren Buffett at Berkshire Hathaway, was his encouragement to investors to build up their inventory of mental models and to use multiple, situation-appropriate models to size up a company or industry.1

Each mental model is meant to simplify the world with a standard model that describes the major features of key underlying dynamics, with the knowledge that every situation or opportunity may differ from the model in important ways. This doesn’t negate the value of the model, as it aids significantly in understanding the general phases of progress, identifying what to look for, and isolating key questions on which to focus. The model shows important features of the topography and potential evolutionary dynamics that may create opportunity or risk, which is clearly of value. It also places great responsibility on understanding how a specific situation—a technology, business model, or industry in this case—is different from the standard model. Insight can still be gleaned, though it is highly context specific and places great value on in-depth research into the history, progress, and development of each technology and industry.

In addition, while this model of the evolution of technology shows the potential path to success, there are numerous points of potential failure along this path. Proper application requires recognizing this truth. For example, many technologies fail to show progress in the proof-of-concept phase. Further, even if proof of concept demonstrates potential, there will be numerous designs and experiments taken to the market with first-generation technology, and not all of these can succeed. Additionally, as we discussed, these first-generation offerings eventually are displaced, if not replaced, by second-generation offerings. Failure travels with success, a fact that Darwin emphasized in his theory of natural selection.

In fact, it is critical to appreciate that typically only one or a few technologies or offerings will break out to success. This dynamic of competing iterations and designs at each phase—with few winners and many losers—means there is risk along with great reward when investing in innovation. The fundamental truth is that the losers in any given field far outnumber the winners over time; therefore, navigating this dynamic is of critical importance.

Furthermore, the timeline of development can vary greatly, with some technologies moving rapidly through these phases, such as digital-based products, apps, or services, while others take decades to develop. There is no common timeline, rather technology evolution is marked by fits and starts, periods of rapid innovation and growth, lulls, and even setbacks. It is in this environment that true long-term investors demonstrate their value-add with patience and perseverance, sticking with innovative companies through the ups and downs.

Especially early on, each progressive movement forward in the development and evolution of a technology will be met with great acclaim, if not outright hype, from entrepreneurs and media alike, only to face the inevitable and quite normal setbacks (what I call “CHIPS”—challenges, hurdles, issues, problems, and setbacks).2 This creates a cycle of hype and disappointment, a rollercoaster of emotion and progress, translated in the financial markets as booms and busts. This is the inherent nature of technology evolution and the financial markets. It will never be tamed and, therefore, must be navigated carefully.

The silver lining is that while booms often are followed by busts, I believe that busts are often followed by new booms! This boom-to-bust-to-boom dynamic can be seen in the dotcom period. Most of us lived through the dotcom boom of the late 90s and the subsequent bust, when the vast majority of dotcoms went out of business. What was lost in the post-script was the dotcom period merely reflected first-generation (Gen 1) technology and the bust reflected the CHIPS/issues (see previous white paper that describes The Technology and Industry Evolution Model for more detail on this process), laying the foundation for the next phase, the second generation (Gen 2). This follow-on period has been called Web 2.0, which led to another wave of growth as Internet and Web technologies finally matured and laid a stronger foundation for higher functionality and superior business models. The evolution of technology naturally leads to boom-bust-boom cycles that are fundamentally driven by Gen 1-to-CHIPS-to-Gen 2 phases in the evolutionary model. This episode demonstrates that in the ashes of many a bust is the phoenix of a new boom.

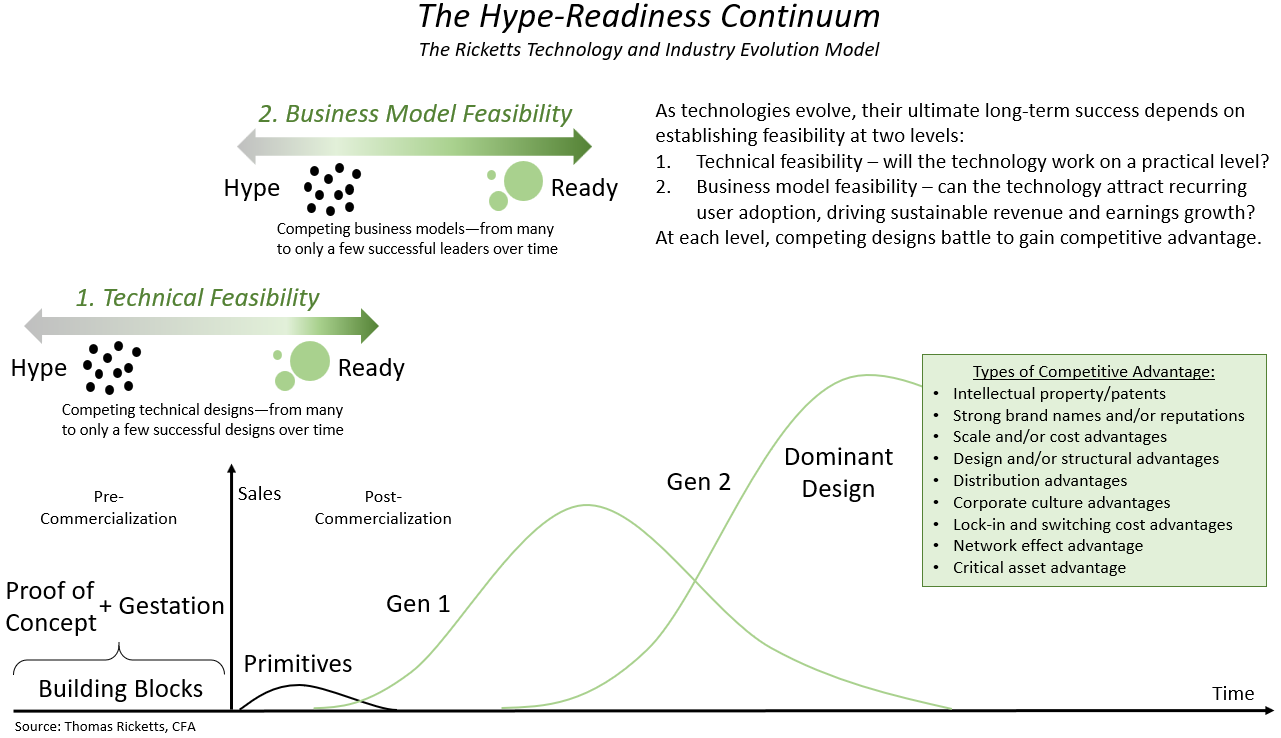

The Hype-Readiness Continuum

Related to the concept of hype is the concept of readiness. Technologies don’t come into the world fully developed and ready for primetime. Instead, their early proof of concept merely shows the long-term potential of the technology, and this is achieved only after numerous iterations and many, many years of development. This gap between the future potential and the current state of the technology creates what I call the Hype-Readiness Continuum (see diagram below). Technologies move along a continuum from Hype to Ready, as the technology improves in performance, functionality, and other important requirements for feasibility.

Furthermore, there actually are two levels of the Hype-Readiness Continuum. The first level is for any new technology to demonstrate technical feasibility. This answers the fundamental question: Will the technology work on a practical level? Just because a new technology shows technical feasibility, doesn’t mean it is ready for consumers. The second level is that a new technology must also establish business model feasibility. This is the level at which the technology demonstrates its ability to survive in the wild, in the marketplace, and for specific use cases and by actual users. At this level, it must answer a second fundamental question: Can the technology attract recurring user adoption, driving sustainable revenue and earnings growth? For technologies to survive and thrive, they must pass through these two levels before succeeding in the marketplace.

Technology Advances Must Be Accompanied by Competitive Advantage to Capture Value

Although our discussion during this three-part white paper series focused on the power of innovation and evolutionary forces, companies are not rewarded for every innovation they generate, even important ones. If new innovations are imitated or copied by competitors, any value that is created is dissipated through competition, leaving only consumers with a surplus. A key complement to innovation then is the ability to capture this value for an extended period of time. Only durable or multiple competitive advantages enable this value capture.

Competitive advantage, alongside innovation, is thus at the core of evolution, both biological and techno-economic. In nature, an individual animal or species with a differential advantage has a preferential path toward higher relative survival compared to other individuals or species. These advantaged species crowd out competitors who lack an advantage and displace them over time. Likewise, competitive advantage is at the heart of industry evolution, as those few companies (and their specific product or service designs) that retain one or multiple competitive advantages take market share from weaker companies over time.

Like organisms, companies must evolve or face extinction. Darwin underlines this dynamic best when he says of species that “we can understand on the principle of competition, and in that of the many all-important relations of organism to organism, that any form which does not become in some degree modified and improved, will be liable to be exterminated. Hence, we can see why all the species in the same region do at last, if we look to wide enough intervals of time, become modified; for those that do not change will become extinct.”3

Types of competitive advantage that companies can build to out-compete competitors include brands, patents, scale, scope, network effects, among many others. I can think of no other exemplar company today that combines as many of these competitive advantages as Amazon. Amazon has built its global brand on bringing the widest selection of products at some of the lowest prices anywhere right to your doorstep. This combination of price, selection, and convenience has never been achieved before. The key is that each additional competitive advantage raises the barrier, or widens the moat, to competitors and entrants. Through consistent innovation and the creation of new advantages, Amazon has become the keystone species in retail and cloud computing.

It is also important to note that competitive advantages are difficult to sustain, precisely because of the evolution of technology, which tends to undermine advantages of leaders in existing or previous generations. As an example, even mighty Wal-Mart has been humbled by the evolutionary shift toward e-commerce and the rise of Amazon. Thus, the evolution of technology within an industry affects the application of using the traditional Porter 5 Forces Model of competitive advantage.4 No question this model is of great value (and I certainly use this important mental model), though the emphasis by users has been too heavily placed on basic competitive or game theory. When technologies, techniques, business models, and industries evolve, these evolutionary dynamics create new rules of competition. Though important, the 5 Forces are not enough. Other forces are at work. Evolutionary and innovation forces are the new gamechangers and must supplement the traditional analysis.

The bottom line is that it is not enough to find an important innovation or evolutionary industry shift when making an investment. These are good starting points, but there are other critical dimensions that must be assessed to filter down to the value-added companies and industries. The evaluation of the evolution of technology is an important new framework, but this must be complemented by other tools in the toolkit, most notably analyzing competitive advantage and business models (and how they evolve), as well as other key factors (such as assessing management, the financials, and the regulatory environment). There is abundant literature on each of these topics, so I won’t provide details on these factors, other than to make clear that while these three white papers touch on powerful evolutionary forces in the world, it in no way negates the importance of other tools, particularly around the assessment of competitive advantage.

In Nature and in Business, Innovation and Evolution Never End

The quote below is of the inspiring parting words at the end of Darwin’s On the Origin of Species. It serves as a great juxtaposition of the organic unfolding of new forms that we see in nature versus the mechanistic world of Newtonian physics that explained the previous Industrial Revolutions.

We can so far take a prophetic glance into futurity as to foretell that it will be the common and widely spread species, belonging to the larger and dominant groups, which will ultimately prevail…whilst this planet has gone on according to the fixed law of gravity from so simple a beginning endless forms most beautiful and most wonderful have been and are being, evolved.

As an investor, I find it harder and harder to apply the mechanistic industrial-era mental models and more intuitive—and profitable—to apply the new biological worldview. Whether one is a growth investor or a value investor, a new dimension has become inescapable and paramount in generating investment insight. In the Age of Innovation and beyond, the ultimate task before every investor is to understand how technologies, product or service offerings, business models, and industries evolve over time. Innovation plus evolution is how investment opportunity is created.

Sources:

- McVagh, Andrew. “What are Mental Models?” My Mental Models: Better Decisions Using A Better Framework website March 2018. https://www.mymentalmodels.info/what-are-mental-models/.

- Ricketts, Thomas. “On Evolutionary Investing.” EvolutionaryTree.com website. White paper. 2017.

- Darwin, Charles. On the Origin of Species. London: John Murray, 1859.

- Porter, Michael. Competitive Strategy: Techniques for Analyzing Industries and Competitors. New York: Free Press, 1980.

Disclosure: These White Papers are meant for informational purposes only. The mention or discussion of specific industries, companies, or stocks in this or other White Papers does not constitute a recommendation to buy, sell, or take other investment action with, a particular security. We reference companies or industries to provide examples of topics being discussed. There can be no assurance that we have owned, currently own, or will own any of the companies or industries mentioned in this or other white papers or articles.

All rights reserved © 2017 Thomas M. Ricketts